Picture this: you’re scrolling through Zillow on a Tuesday night, eyeing a beautiful four-bedroom in Short Pump or a charming craftsman near the Oceanfront in Virginia Beach. The listing price looks manageable. Your income is solid. But then that number creeps into your head: twenty percent down. On a $400,000 home, that’s $80,000 in cash before you even think about closing costs. You close the tab. You tell yourself you’ll revisit it “when you’re ready.”

Here’s the truth: that moment of hesitation is costing Virginia homebuyers real opportunities every single day. And it’s based on a myth.

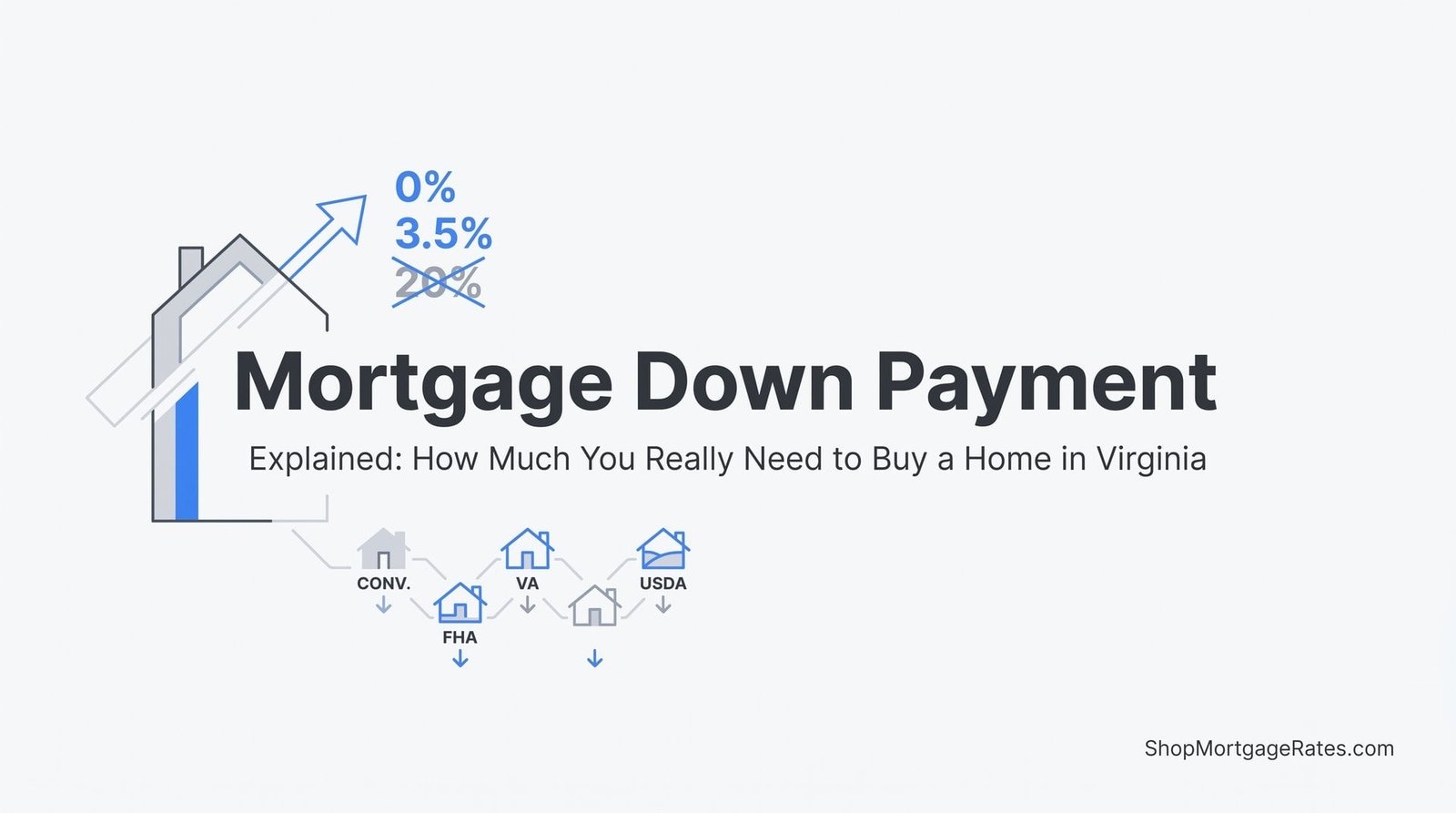

The 20% down payment rule is not a law, not a requirement, and for most loan types, not even close to the actual minimum. Depending on your situation, you could buy a home in Richmond, Fredericksburg, Charlottesville, or Chesapeake with as little as 3% down, 3.5% down, or even nothing at all. The key is knowing which loan type fits your profile and working with a mortgage professional who has access to enough lenders to actually find you the best deal.

That’s exactly what ShopMortgageRates.com does. As a Mortgage Broker of the Year with access to hundreds of wholesale lenders, ShopMortgageRates.com serves homebuyers across Virginia, Florida, Tennessee, and Georgia, helping them cut through the noise, compare real options, and get into homes faster than they thought possible. And the best part? You can start exploring your options with zero impact to your credit score.

This article breaks down everything you need to know about the mortgage down payment: what you actually need, how it affects your monthly costs, how to save smarter, and why the lender you choose matters more than most buyers realize.

The 20% Myth and What Virginia Homebuyers Actually Put Down

The 20% down payment expectation has been around for decades, and it persists for a reason: it’s the threshold that eliminates private mortgage insurance on a conventional loan and signals strong financial footing to lenders. Real estate agents mention it. Parents repeat it. Financial media reinforces it. So buyers in growing Virginia markets like Henrico, Chesterfield, Midlothian, and Short Pump hear “20%” so often that they assume it’s the only path forward.

It isn’t. Here’s what the actual minimums look like by loan type.

Conventional Loans (as low as 3% down): Through programs like Fannie Mae’s HomeReady and Freddie Mac’s Home Possible, qualified buyers can put down as little as 3% on a conventional loan. These programs are designed for first-time buyers and moderate-income households, and they’re widely available through lenders in Virginia. Many of these buyers also benefit from first time homebuyer programs that offer additional assistance.

FHA Loans (3.5% down): Backed by the Federal Housing Administration, FHA loans require just 3.5% down for borrowers with a credit score of 580 or higher. They’re more flexible on credit history than conventional loans, making them a popular choice for buyers who are still building their financial profile. Understanding the differences between FHA vs conventional loans can help you decide which path is right for you.

VA Loans (0% down): For eligible active-duty service members, veterans, and surviving spouses, VA loans offer 100% financing with no down payment required. Virginia has one of the largest veteran populations in the country, and this benefit is one of the most powerful tools available to qualified buyers across Hampton Roads, Newport News, and beyond.

USDA Loans (0% down): The USDA Rural Development loan program also offers zero-down financing for buyers purchasing in eligible rural and suburban areas. In Virginia, counties like Goochland, Louisa, Caroline County, and the Lake Anna area frequently include USDA-eligible properties. Buyers should verify specific property eligibility using the USDA eligibility map, but the opportunity is real and often overlooked.

Now, a word about PMI. Private mortgage insurance is required on conventional loans when your down payment is less than 20%. It typically costs between 0.5% and 1.5% of your loan amount annually, added to your monthly payment. That sounds like a drawback, and it is a cost worth understanding. But PMI is not permanent. On conventional loans, it can be removed once your equity reaches 20%, and it automatically terminates at 22% equity under federal law.

The math often favors buying sooner with a smaller down payment rather than waiting years to save 20%. Every month you wait, you’re paying rent instead of building equity, and in markets like Midlothian or Hanover where prices have been moving, the home you’re saving toward may cost more by the time you get there. PMI is a temporary cost. Waiting has its own price tag.

How Your Down Payment Shapes Your Monthly Payment in Virginia

Understanding the relationship between your down payment and your monthly costs is one of the most practical things you can do before you start shopping. Let’s walk through how the numbers shift based on how much you put down.

Imagine a home priced in the range common to markets like Fredericksburg, Spotsylvania, or Charlottesville. On a $350,000 home with a 30-year fixed conventional loan, here’s how different down payment amounts change the picture. Using a home loan calculator can help you model these scenarios with real numbers.

3% down ($10,500): Your loan amount is $339,500. You’ll have PMI added to your payment until you reach 20% equity, and your monthly principal and interest payment will be at its highest of these scenarios. But your out-of-pocket cost to get into the home is dramatically lower.

5% down ($17,500): Your loan amount drops to $332,500. PMI is still in play, but slightly reduced. Your monthly payment comes down modestly compared to the 3% scenario.

10% down ($35,000): Loan amount is $315,000. PMI is still required but at a lower rate since your loan-to-value ratio has improved. Your monthly payment is meaningfully lower, and you’ll reach the 20% equity threshold faster.

20% down ($70,000): Loan amount is $280,000. No PMI. Your monthly payment is the lowest of these scenarios, and you’ll pay significantly less in total interest over the life of the loan. But you’ve also deployed $70,000 in cash upfront.

The relationship between down payment size and loan-to-value ratio also affects the interest rate you’re offered. A lower LTV signals less risk to lenders, which can translate to a better rate. However, the difference in rate between a 5% and 20% down payment is often smaller than buyers expect, and that gap has to be weighed against the opportunity cost of tying up tens of thousands of dollars in a down payment instead of keeping it liquid or invested. Learning how to lock in the lowest mortgage rates can help you maximize savings regardless of your down payment size.

This is exactly where working with a mortgage broker like ShopMortgageRates.com creates a real advantage. A retail lender like Rocket Mortgage or Freedom Mortgage can only offer you their own rate on their own products. ShopMortgageRates.com shops across hundreds of wholesale lenders to find the rate-and-down-payment combination that actually makes sense for your situation, not just the one product that lender happens to sell. That difference in access can translate to a meaningfully lower monthly payment over the life of your loan.

Why ShopMortgageRates.com Outperforms Rocket Mortgage, Fairway, and the Local Competition

Let’s be direct about how the mortgage industry works, because most buyers don’t realize there are fundamentally different types of mortgage companies, and the type matters enormously to your outcome.

Retail lenders like Rocket Mortgage, Freedom Mortgage, and PrimeLending are direct lenders. They originate loans using their own money and their own guidelines. When you apply with them, you’re getting one set of products from one company. They may have competitive rates on certain loan types, but they cannot offer you anything outside their own product menu. If their down payment requirements or rate on a given day don’t work for your profile, your only option is to walk away. Understanding how to go about choosing a mortgage lender is one of the most important decisions you’ll make in this process.

Fairway Independent Mortgage and CapCenter operate similarly. They’re established names with strong marketing, but their loan officers are selling their company’s products. That’s a fundamental limitation when you’re trying to find the lowest possible down payment paired with the best available rate.

Local Virginia lenders like Alcova Mortgage, Atlantic Bay Mortgage, C&F Mortgage Corporation, River City Lending, and Southern Trust Mortgage are solid, reputable companies with genuine Virginia roots. But most operate as correspondent lenders or with a limited panel of investors. They’re not shopping hundreds of lenders on your behalf. They’re working within their own network.

ShopMortgageRates.com operates as a mortgage broker, which means something specific and important: rather than offering you one company’s products, we access hundreds of wholesale lenders and find the option that fits your down payment, credit profile, and rate goals. The Mortgage Broker of the Year recognition isn’t just a badge; it reflects a model that is structurally built to serve the borrower, not the lender.

Now here’s a differentiator that matters even before you choose a loan: the Free NoTouch Credit Solution.

When you reach out to Movement Mortgage, CrossCounty Mortgage, Guild Mortgage, NFMLending, Embrace Home Loans, Penny Mac, or most other retail lenders for a rate quote or pre-qualification, they typically run a hard credit inquiry. That pull shows up on your credit report and can temporarily lower your credit score. If you’re shopping around and talking to multiple lenders, those inquiries add up. With ShopMortgageRates.com’s soft credit pull mortgage approach, you avoid that risk entirely.

At ShopMortgageRates.com, the pre-qualification process uses a soft credit pull, which means zero impact to your credit score. You can find out exactly what loan programs you qualify for, what your real down payment options look like, and what rate range you’re working with, all without touching your credit. That’s a meaningful difference, especially for buyers who are still in the planning phase or protecting their score for a competitive purchase offer.

Veterans United is another name worth addressing directly. They specialize in VA loans and do it well. But they are a single lender. If you’re a veteran in Virginia Beach, Newport News, or Hampton Roads, you deserve to know whether a broker with access to multiple VA lenders can find you a better rate or terms than one company’s offering. With ShopMortgageRates.com, you get that comparison built in.

Smart Down Payment Strategies for Virginia Buyers and Beyond

Knowing the minimum down payment requirement is one thing. Having the cash ready is another. Here are practical, realistic strategies for building your down payment, tailored to what actually works for buyers in Virginia and in the other states ShopMortgageRates.com serves: Florida, Tennessee, and Georgia.

Automate your savings: Set up a dedicated savings account and automate a fixed transfer every payday. Treating your down payment fund like a non-negotiable bill is the most consistent way to build it. Even modest monthly contributions compound meaningfully over 12 to 24 months.

Use gift funds strategically: Most loan programs allow a portion or all of your down payment to come from a gift from a family member. FHA loans are particularly flexible here. The key requirement is documentation: the donor must provide a gift letter confirming the funds are not a loan, and lenders will want to see the transfer. If a family member wants to help you get into a home in Stafford, Prince William, or Hanover, this is a legitimate and widely used path.

Tap retirement accounts carefully: Some loan programs and IRS rules allow first-time homebuyers to access retirement funds for a down payment with reduced or waived penalties. This is worth exploring with a financial advisor, but it comes with real trade-offs: you’re reducing your long-term investment balance and potentially triggering tax obligations. Use this option with full awareness of the costs.

Know your target market’s price range: Your down payment goal should match the market you’re buying in. Hampton Roads, Newport News, Chesapeake, Suffolk, Williamsburg, and Yorktown each have distinct price ranges that differ from Roanoke or Lynchburg. A 3% down payment on a home in one market may be a very different dollar amount than in another. Getting pre-qualified early means you’re saving toward a real number, not a guess. You can check your mortgage eligibility without any impact to your credit score to start setting that target.

For buyers in Florida, Tennessee, and Georgia, ShopMortgageRates.com brings the same access to hundreds of lenders and the same no-credit-hit pre-qualification to your homebuying process. Markets in those states have their own dynamics, but the core advantage is identical: a broker who shops the market for you rather than selling you one product.

The single most actionable step in any down payment strategy is getting pre-qualified early. When you know exactly what loan programs you qualify for and what down payment is actually required for your situation, you can set a precise savings target and move with confidence. Understanding the full mortgage approval process from pre-qualification to closing helps you plan each step with clarity. ShopMortgageRates.com’s Free NoTouch Credit Solution makes that first step completely risk-free.

Your Biggest Down Payment Questions, Answered Head-to-Head

Can I really buy a home with zero down in Virginia?

Yes, through two specific programs. VA loans are available to eligible veterans, active-duty service members, and surviving spouses with no down payment required. USDA loans offer zero-down financing in eligible rural and suburban areas, including parts of Goochland, Louisa, Caroline County, and the Lake Anna region. Both programs are legitimate, widely used, and available through ShopMortgageRates.com’s lender network. You can explore your options further on our zero down payment mortgage page.

Why use a broker instead of Veterans United or UWM?

Veterans United is a single lender specializing in VA loans. UWM (United Wholesale Mortgage) is a wholesale lender that works through brokers, not directly with consumers. When you work with ShopMortgageRates.com, you get access to multiple VA lenders, including wholesale channels, which means genuine rate competition rather than one company’s pricing. For Virginia veterans comparing their options, understanding the differences between a VA loan vs FHA is also essential to making the right choice.

Will checking my rate hurt my credit score?

Not at ShopMortgageRates.com. The Free NoTouch Credit Solution uses a soft pull for pre-qualification, which has zero impact on your credit score. Most retail lenders require a hard inquiry just to give you a rate quote. That difference matters when you’re in the planning phase or when your credit score is a factor in the rate you’ll receive.

What’s the difference between a down payment and closing costs?

Your down payment is the portion of the purchase price you pay upfront toward the home itself. Closing costs are separate fees associated with processing the loan and completing the transaction, including things like title insurance, appraisal fees, lender fees, and prepaid items like homeowners insurance. Both require cash at closing, so your total cash-to-close figure is always higher than the down payment alone. Our detailed guide on mortgage closing costs breaks down exactly what to expect so you can budget accurately.

How does my down payment affect my ability to compete in a hot market like Hanover, Stafford, or Prince William?

In competitive markets, sellers and their agents pay attention to the strength of your offer, and a larger down payment can signal financial stability. However, a strong pre-qualification letter from a credible lender matters just as much. Knowing your exact down payment options and having documentation ready through ShopMortgageRates.com’s pre-qualification process puts you in a position to move quickly and confidently when the right home comes available.

Unlike Prosperity Mortgage, RatePro Mortgage, or other competitors in the Virginia market, ShopMortgageRates.com combines three things that most lenders simply cannot offer together: Mortgage Broker of the Year recognition, access to hundreds of lender options, and a no-credit-hit pre-qualification process. For Virginia homebuyers, that combination is genuinely rare.

Your Next Steps Start Here

The mortgage down payment doesn’t have to be the wall standing between you and homeownership in Virginia. As this article has shown, the real minimums are far lower than most buyers assume, the right loan type can eliminate the down payment entirely for eligible borrowers, and the broker you choose has a direct impact on the options available to you.

Here’s what to take away. You likely need less cash upfront than you think. VA and USDA loans offer genuine zero-down paths for eligible buyers. PMI is a temporary cost, not a permanent penalty. And working with a broker who shops hundreds of lenders will almost always outperform going directly to a single retail lender, whether that’s Rocket Mortgage, Fairway, Alcova, or any other company with a limited product menu.

The smartest first move is also the lowest-risk one: get pre-qualified with no impact to your credit score and find out exactly what you qualify for today. Whether you’re buying in Richmond, Virginia Beach, Fredericksburg, Charlottesville, Roanoke, Lynchburg, or anywhere across Virginia, Florida, Tennessee, or Georgia, ShopMortgageRates.com is ready to shop the market for you.

Visit ShopMortgageRates.com to learn more about our services, start your free no-touch pre-qualification, and connect with the Mortgage Broker of the Year team that has helped buyers across Virginia find the down payment solution that actually fits their life.